The Strait of Hormuz has been effectively closed for a month—the first time in modern history. Its impact on markets has been broad, its resolution remains uncertain, and the range of possible outcomes is unusually wide. Through our Needs, Means, & Seams framework, we examine what this situation means for clients and why proactive diversification remains a durable form of protection.

Since February 28, the Strait of Hormuz—through which roughly one-fifth of global oil, liquefied natural gas, and critical industrial commodities ordinarily flow—has been effectively cordoned off. What began with coordinated U.S.-Israeli strikes on Iranian military infrastructure escalated as Iran’s Revolutionary Guard Corps shut the waterway to international shipping.

Maritime traffic has collapsed by more than 90%, with some 2,000 ships stranded on either side. President Trump has extended his deadline for Iran to reopen the channel amid fragile and, at times, contradictory negotiations.

The market response through March has been consistent with a broad repricing of risk. Equities have sold off, the U.S. dollar has strengthened as investors sought safety in the world’s reserve currency, bond yields have crept higher on concerns over more persistent inflation, and credit spreads have widened. While geopolitical events tend to follow a familiar arc—an initial sell-off, uncertainty, and an eventual recovery—the Strait of Hormuz has some unique qualities, not because of the conflict itself, but because of what flows through it.

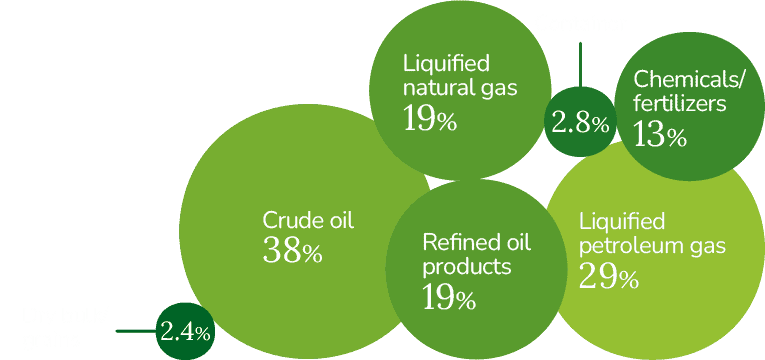

As demonstrated in Figure 1, the waterway’s importance extends well beyond oil. The Gulf region produces nearly half the world’s urea and roughly 30% of global ammonia—key fertilizer inputs, which we use as an illustrative example below—along with significant volumes of helium, aluminum, sulfur, and petrochemicals. The International Energy Agency has described the situation as the largest oil supply disruption in history, and while that is a significant statement, the practical effects are being partially offset by strategic reserve releases and rerouting that have kept markets functioning, if under strain.

The scale of the disruption explains the market reaction; the difficulty lies in gauging how long it lasts. What has compounded the uncertainty is the difficulty in reading the situation’s trajectory. The U.S. administration’s messaging has been inconsistent—from threats to destroy Iranian power infrastructure, to claims of productive negotiations, to extended deadlines—making it challenging for markets to price a resolution with any confidence. That ambiguity has been as much a source of volatility as the physical disruption itself.

Oil is the most visible disruption, and as the first link of an integrated supply chain, the knock-on effects follow from there. Crude oil is refined into petrochemicals that produce nitrogen-rich fertilizer; that fertilizer grows corn; corn becomes livestock feed; feed raises cattle and poultry; and consumer protein eventually reaches grocery shelves.

Every degree of separation adds time before markets can normalize. It is worth noting, however, that many of these downstream effects remain in their early stages—and their severity depends almost entirely on how long the disruption persists. A swift resolution might allow supply chains to recalibrate more readily than headlines suggest, while a prolonged closure could compound the pressure at each successive stage.

Some relief has come through alternative pipeline routes moving approximately nine million barrels per day. While less than half the Strait’s normal throughput, it remains a meaningful offset that, together with strategic reserves, has helped prevent worst-case scenarios from materializing thus far.

| Market Statistics | Month-to-Date | Year-to-Date |

|---|---|---|

| S&P 500 | -4.98% | -4.35% |

| Russell 2000 | -5.01% | 0.92% |

| MSCI EAFE Index | -10.73% | -1.09% |

| U.S. Agg. TRBI | -1.76% | -0.05% |

| U.S. Dollar Index | 99.96 pts (+235 pts) | +164 pts |

| WTI Crude (USD/bbl) | $101.38 (+$34.49) | +$44.38 |

| Gold (USD/oz) | $4,668 (-$611) | +$349 |

In our most recent Quarterly Insights, we introduced this framework to examine how capital allocation is shaped by structural demand, the resources available to meet it, and the fault lines between them. The current environment provides a useful application.

The commodities flowing through the Strait are not discretionary—they are embedded in food production, semiconductor manufacturing, and heavy industry. What this crisis has exposed is less about the disruption itself and more about the structural vulnerability of concentrating so many essential inputs through a single 21-nautical-mile corridor.

The short-term workarounds to mobilize commodities are functional but perhaps unsustainable, and the more meaningful development may be what’s happening beyond them. Taiwan is restarting nuclear reactors, India has signed a new uranium supply agreement with Canada’s Cameco, and capital is flowing into North American small modular reactor projects. We can, in a sense, read these developments as the global economy’s own version of correcting insufficient diversification in real time.

The gap between what the world requires and how it can currently access those resources has created enormous dispersion across markets—Gulf producers under pressure while North American peers earn a premium, gold defying safe-haven expectations as dollar strength takes precedence, central banks caught between inflationary risks and slowing growth. That breadth of dispersion across asset classes, geographies, and sectors is precisely where diversification can earn its keep.

This is not an easily tradable event because the range of outcomes is so vast. The conflict could be resolved in days, or it may endure for months. A withdrawal of U.S. forces would likely prompt a broad market rally—even if the Strait remained closed and infrastructure damage lingered. While energy prices might remain elevated, investor sentiment could improve well ahead of the fundamentals. Conversely, an escalation or prolonged standoff would deepen the pressures we’ve described.

Like many others, our working thesis has been that the Republican Party can ill afford a long, drawn-out conflict given the unpopularity of high gasoline prices and a costly war with voters as they head into midterm elections this fall. The U.S. administration’s objectives, however, have been difficult to pin down; what constitutes a successful operation has shifted repeatedly, making it harder for investors to calibrate expectations around duration or resolution

This scenario is where diversification demonstrates its value as a proactive, deliberate choice rather than a passive default. Market segments have reacted differently to this unfolding crisis, and they are likely to exhibit equally distinct responses to its resolution depending on what form it takes. Shipping lanes could reopen the same day hostilities cease, or they could remain obstructed for far longer. North American energy producers may respond well to one scenario, European industrials to another, and fixed income to another still. Given the sheer number of possibilities, timelines, and variables at play, diversification distributes risk across outcomes rather than relying on any specific one breaking in the right direction.

Such approaches are not devised in anticipation of conflict—they are designed ahead of time to prioritize risk management, diversified income streams, and the kind of global breadth that disperses exposure rather than localizes it.

Strategies following this philosophy likely safeguarded capital better than broader indices (as seen in the Market Statistics table) throughout this disruption, allowing advisors to opportunistically rebalance portfolios on behalf of clients—to take profits where prices have surged while acquiring quality at reduced valuations.

As Figure 2 illustrates, markets have historically found their footing once the smoke of uncertainty begins to clear—and for all its differences from past flareups, this event remains a geopolitical one. The investments and infrastructure decisions being made today—by nations diversifying energy sources, by companies seeking more reliable supply chains—are laying the groundwork for what comes next.

The realm of possibility is wide. Strategies built on diversification, income, and fundamentals are not confined to a single outcome—they are positioned to navigate whichever one arrives.